By Alton Tabereaux, Contributing Editor.

The European primary aluminum industry has been deeply impacted by surging energy prices. This is due to a combination of factors, including increasing demand, skyrocketing natural gas prices, and insufficient quantities of affordable renewable (wind, solar, hydro) or nuclear energy. The invasion of Ukraine also significantly impacted supply chains, in particular the supply of natural gas, which further exacerbated the problem. In the wake of these challenges, energy-intensive industries, such as aluminum, are closing or temporarily suspending their European operations.

Surging Inflation and Energy Prices

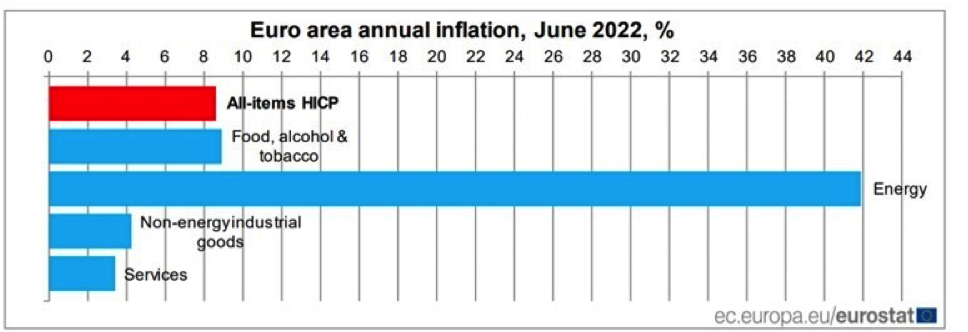

As of June 2022, the inflation rate in the European Union (EU) was at 8.6% (Figure 1), up from 8.1% in May, based on estimates from Eurostat,1 the statistical office of the EU. Prices are rising fastest in Estonia, which had an inflation rate as high as 20.1%. The current rate of inflation in the EU is higher than it’s been since July 2008, when prices were growing by 4.4% year-on-year. Before the recent rise in inflation, price increases in the EU had been maintained at relatively low levels, with the inflation rate remaining below 3% between January 2012 and August 2021. As Figure 1 shows, energy showed the highest annual rate of inflation in June 2022 (41.9%, compared with 39.1% in May 2022).

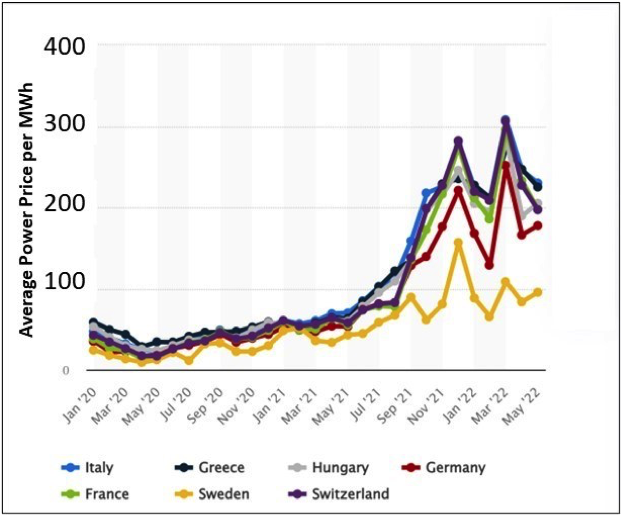

Electricity prices (€/MWh) increased across the EU due to a combination of factors, but were mostly caused by high natural gas prices and increasing demand. Natural gas prices were exorbitant in European countries during the last six months of 2021 and continued into 2022 (Figure 2). The rapid increase in energy prices during this period was due to the difference in the mix of natural gas, oil, coal, and renewable energies across European countries. When there were insufficient quantities of less expensive renewable energy (wind, solar, and hydro) available, then expensive natural gas was used to make up the difference during periods of high energy demand.

Despite the increased demand, gas pipelines that supply Europe from countries such as Russia, Norway, and Algeria have not increased the amount of natural gas being delivered, despite the higher price. Rather, they have kept their supplies at the regular natural gas volumes. Combined with low gas storage in Europe and increased demand in Asia during the 2021 winter, prices surged even higher.

Of all the European countries, Sweden had the lowest average price in 2021 and 2022. This is because hydropower and nuclear power generation were the main sources of electricity in Sweden in 2019, each accounting for a 39% share of the country’s supply. Sweden is one of the global leaders in decarbonization, with clean energy sources—including hydropower, nuclear, wind, and solar—representing more than 90% of the country’s electricity mix.

The Effect of Carbon Prices

Some EU countries have blamed rising energy costs on the EU’s carbon price, which is run by the Emissions Trading System (ETS) and is the region’s financial mechanism for curbing emissions. When companies pollute, they are forced to buy carbon permits to continue operating. EU carbon prices have risen sharply since hitting €50 per tonne for the first time in May 2021. In January 2022, the EU carbon price fluctuated between €80 and €90 per tonne, and it is projected that the price could reach as high as €100 per tonne.

However, the EU carbon pricing scheme does allow for national governments to award compensation to energy intensive industries, such as aluminum smelting. This compensation is aimed at helping them recoup some of the costs relating to high carbon prices that are paid to the ETS. For example, in Germany, the compensation (offsetting the carbon price) for a smelter producing 200,000 tpy would be about €67.55 million (US$72.54 million).

Impact of the War in Ukraine

Russia invaded Ukraine on February 24, 2022. Many European countries stepped in and supplied military support to Ukraine, along with crucial assistance to millions of refugees. Western leaders have also imposed a series of sanctions on Russian oil and gas following the invasion of Ukraine. There are warnings that Russia may stop supplying gas to Europe in retaliation. Thus, the European Union is currently working to reduce their consumption of Russian oil and natural gas.

As a major player in global energy markets, Russia is one of the world’s top three crude producers, competing for the top spot with Saudi Arabia and the U.S. Russia relies heavily on revenues from oil and natural gas, which in 2021 made up 45% of the country’s federal budget. It is also the world’s largest gas exporter. In 2021, the country produced 762 billion m3 of natural gas and exported approximately 210 billion m3 via pipeline.

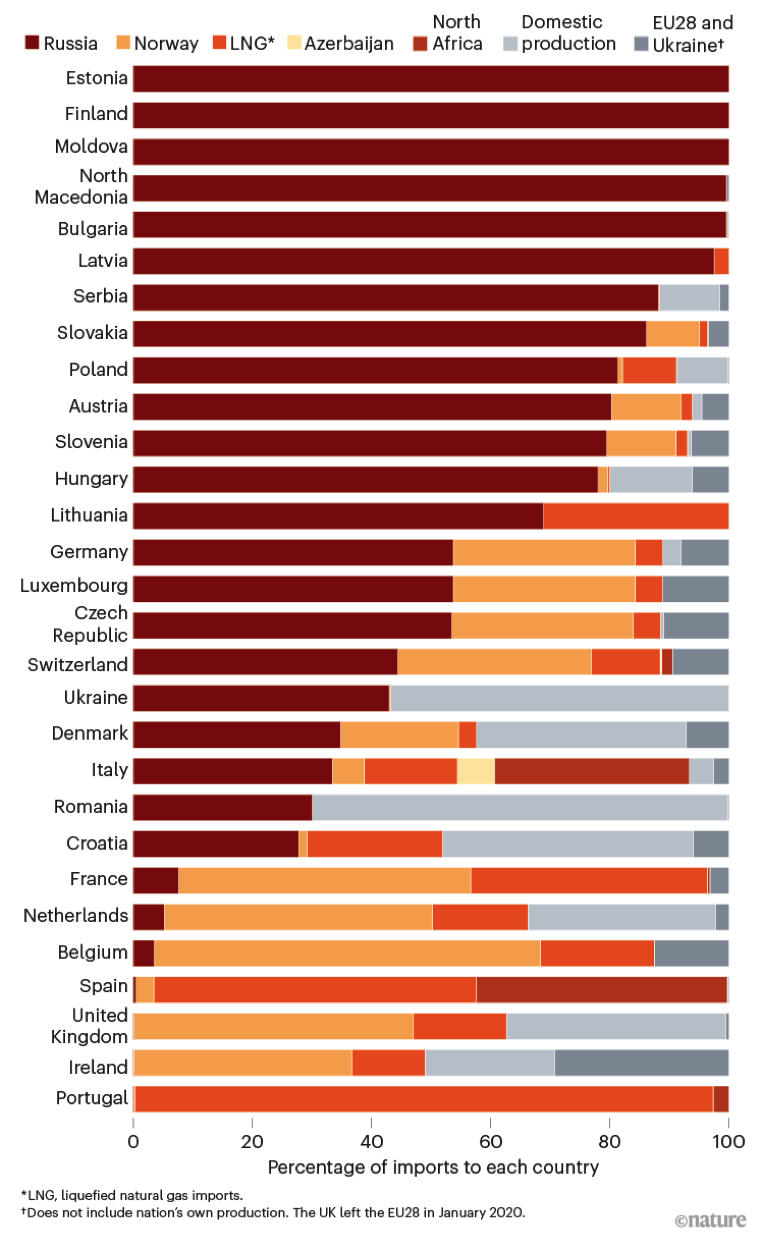

Russia supplied around 45% of the EU’s natural gas in 2021, with the EU importing a total of 155 billion m3 for the year. This includes around 140 billion m3 delivered via pipeline and another 15 billion m3 delivered in the form of liquefied natural gas (LNG). Imports from Russia represented almost 40% of its total gas consumption in 2021. However, a number of individual European countries receive a much larger proportion of their annual natural gas from Russia (Figure 3).2 Estonia, Finland, Moldova, North Macedonia, and Bulgaria receive 100% of their natural gas from Russia, while Germany received about 50% and the U.K., Ireland, and Portugal did not receive any natural gas from Russia.

Germany is a major importer of natural gas and has the continent’s largest economy. Therefore, the energy crisis is particularly acute in Germany, which relies on Russia for roughly half of its natural gas and coal and for more than one-third of its oil. That changed with the Russian invasion, when already high prices soared from €90/MWh to over €300/MWh. Germany’s immediate challenge is to reduce reliance on natural gas in the power-generation sector, which is further complicated by the country’s exit from nuclear power (its last three nuclear stations are scheduled to close this year). On February 22, 2022, Germany stopped its approval of a newly built gas pipeline from Russia and is now planning to import LNG from countries such as Qatar, Japan, South Korea, and the U.S.

Gas import contracts with Gazprom, a Russian majority state-owned energy corporation, are set to expire by the end of 2022. These contracts cover more than 15 billion m3 per year, equating to around 12% of the company’s gas supplies to the EU in 2021. Overall, contracts with Gazprom (covering close to 40 billion m3 per year) are due to expire by the end of this decade. Analysis indicates that production of natural gas inside the EU and imports from non-Russian pipelines (including from Azerbaijan and Norway) could increase over the next year by up to 10 billion m3 from 2021 numbers.

The Russian invasion of Ukraine resulted in energy prices continuing at elevated levels in European markets, supported by increased fears of disruption to gas flows. In response, the European Commission published its REPowerEU plan,3 which aims to make Europe independent of Russian fossil fuels before 2030. Independence from Russian gas is expected to strengthen EU demand for renewable energy and hydrogen, supporting Norsk Hydro’s ambition to grow in new, more sustainable energy. REPowerEU focuses several measures, including saving energy, diversifying supplies by working together with international partners, accelerating the rollout of renewable energy, reducing fossil fuel consumption in industry and transport, and additional funding for research and innovation projects.

Fluctuating Aluminum Prices

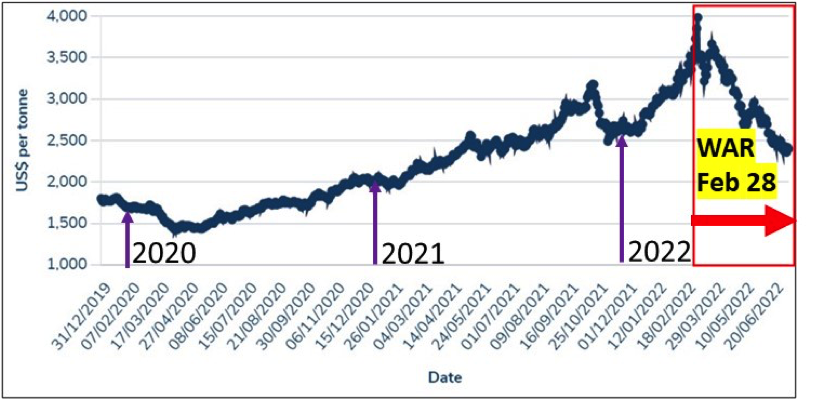

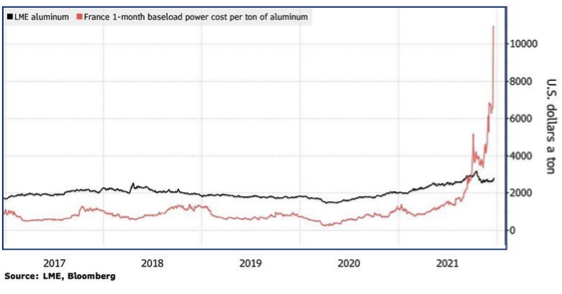

In 2021, prices for aluminum on the London Metal Exchange (LME) reached an annual average of US$2,480/tonne, a 46% increase from 2020, when the average price was US$1,704/tonne. The highest LME value in 2021 was US$3,180/tonne, as recorded in October (Figure 4).

During the first quarter of 2022, the three-month LME aluminium price increased from US$2,808/tonne to US$3,491/tonne. This price increase was due in part to the invasion of Ukraine, which increased fears of sanctions on Russian producers and significant disruptions to metal flows. In addition, rising gas and power prices have led to an increase in production costs in Europe, followed by several smelter curtailments.

Now that China’s 2020-2021 winter power crunch has passed, the country is expected to start ramping up aluminum production at its smelters. LME prices are expected to decrease in 2022 and 2023 as a result of China’s increasing aluminum production, which is expected to grow at a rate of 1 million tpy, as it has done for the past three years. National aluminum output in China rose from 36.0 million tonnes in 2019 to 37.1 million tonnes in 2020 and 38.5 million tonnes in 2021. In the next five years, China aims to boost its share of renewable energy usage to about 20% of its energy consumption, up from about 15% currently.

Decreasing Aluminum Production

Since aluminum smelting is an energy-intensive business, Europe’s smelters were struggling with elevated power pricing even before Russia’s invasion in Ukraine further impacted prices. With the CO2 certificate quotations surging in 2021, reflecting the record-high energy costs, European aluminum producers faced a 300% increase in electricity bills in the second half of 2021 and 2022, compared to the same period in 2020. While aluminum prices increased by more than 40% in 2021-2022 and demand for primary aluminum products is booming, profitability was being eroded by the far greater surge in power prices over the same time period (Figure 5).

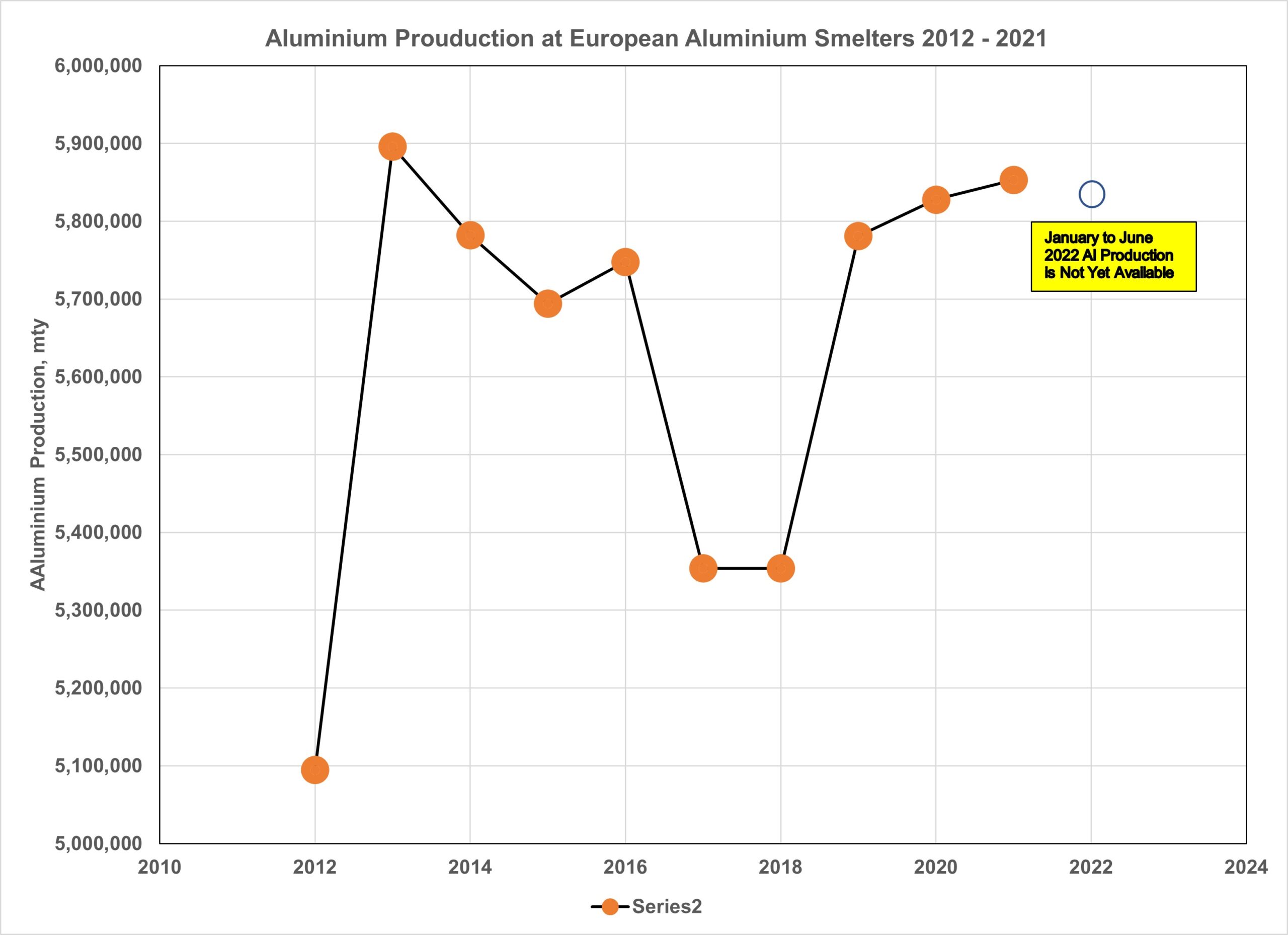

Facing these soaring energy costs, Europe’s primary aluminum smelters are continuing to curtail production. The region’s output of aluminum metal has fallen by 1.14 million tonnes over 2021 and 2022, with the slide still accelerating just before power prices started moving upwards (Figure 6). Except for only three years (2012, 2017, and 2018), the average aluminum production for the European countries has been consistent at an average of almost 5.8 million tpy.4 Some of the major curtailments and closures are noted in alphabetical order hereafter.

Alcoa announced a two-year closure of its San Ciprián aluminum smelter in Spain in response to the jump in the cost of power in recent years. The company came to an agreement with the labor force at the plant regarding the closure. The plant will begin closure activities for halting its 228,000 tpy smelter. These activities will continue through the end of December 2023.

The 150,000 tpy Aldel aluminum smelter in Delfzijl, the Netherlands, halted production in October 2021. According to the company, the cost of electricity was about €4,500/tonne of aluminum, while the aluminum selling price was around €2,500/tonne. Adel was the only producer of primary aluminum in the Netherlands, with an annual production capacity for 110,000 tonnes of primary aluminum and 50,000 tonnes of recycled aluminum.

The 283,000 tpy ALRO Slatina aluminum smelter in Romania was closed in January 2022 due to a shortage in electricity supply and rising costs. Existing energy contracts were denounced or renegotiated at inflated costs. The company stated that they could not produce aluminum at the price of US$2,300-2,600/tonne. In addition, ALRO is halting production at Alum Tulcea, its calcined alumina refinery facility, which is also the only producer of calcined alumina in Romania. As of August 1, the company will halt refinery activities due to the price of electricity and natural gas. The plant had a production capacity of 600,000 tpy. The alumina was delivered to the ALRO Slatina alumina smelter, with only a small quantity for export.

The 285,000 tpy Aluminium Dunkerque (part of ALVANCE Aluminium Group) aluminum smelter in France announced that it would reduce output by 15% in response to a surge in power prices. The cuts equate to about 3% of the smelter’s total production capacity. The plant reported that it has lost about €20 million (US$22.6 million) since the beginning of November, and further curtailments may be necessary, if power prices remain at such exorbitant levels.

The 120,000 tpy Podgorica PKA aluminum smelter in Montenegro was fully idled by the end of 2021, when rising electricity prices made its production uneconomical. Preparation works for the gradual halt in production began on December 15 due to the increased electricity price set by power company EPCG, which was expected to begin in January 2022. KAP had previously been paying a price of €45/MWh. EPCG first offered a price of €120/MWh, followed by an even higher price of €127/MWh.

The Slovalco aluminum smelter in Slovakia, majority owned by Norsk Hydro, announced that it would cut its output to around 60% of capacity, about 70,000 tonnes. As a result, the smelter produced only 114,581 tonnes in 2021. The reduced production was in response to high electricity costs, which were reported to be €150/MWh, three times higher than the previous year. Slovalco is Central Europe’s only smelter, with an annual capacity of 175,000 tonnes of aluminum products. After shutting 47 pots in late 2021, the smelter shut down an additional 44 pots. It now has 135 out of 226 pots in operation. In August 2022, Slovaco announced that it would close the smelter, as there was no sign of improving energy prices. The closure will be completed by the end of September 2022.

Trimet in Germany cut aluminum production by 30% at its 135,000 tpy Hamburg smelter and 165,000 tpy at its Voerde smelter, as of January 2022. In March 2022, the company announced that it would further cut aluminum production at its Essen facility by 50%, due to higher energy prices after Russia invaded Ukraine. The company noted that before electricity prices jumped in Europe, power accounted for about 40% of smelting costs. However, that figure has grown substantially.

Despite the energy challenges, one smelter has been investing in restarting production. The Portovesme smelter in the Sardinian Region of Italy originally ceased production in 2012 and was sold by Alcoa to the Italian-Swiss company Sider Alloys. In October 2021, Sider Alloys received approval to reconstruct the 155,000 tonne smelter and announced it would enact a €150 million investment plan to restart the smelter. As of March 2022, the company was preparing to start up the first section of the smelter, while the rest of the refurbishment was being completed.

References

- “Annual inflation up to 8.6% in the euro area,” Eurostat, July 2022.

- Tollefson, Jeff, “What the war in Ukraine means for energy, climate and food,” Nature, Vol. 604, April 5, 2022, pp. 232-233.

- “REPowerEU: A plan to rapidly reduce dependence on Russian fossil fuels and fast forward the green transition,” European Commission, May 18, 2022.

- Pawlek, Rudolf, Primary Aluminum Tables, Light Metal Age, 2021-2022.

Dr. Alton Tabereaux is a technical consultant in resolving issues and improving productivity at aluminum smelters since 2007. He worked for 33 years as a manager of research and process technology for both Reynolds and Alcoa Primary Metals. He was recipient of JOM Best Technical Paper Award in 1994 and 2000, editor of Light Metals in 2004, and received the TMS Light Metals Distinguished Service Award in 2007. He has been a lecturer at the annual International Course on Process Metallurgy of Aluminium held in Trondheim, Norway, and an instructor at the annual TMS Industrial Aluminum Electrolysis Courses. He has published over 65 technical papers and obtained 17 U.S. patents in advances in the aluminium electrolysis process. He participated as a consultant in an EPA sponsored “Asian-Pacific Partnership” program to minimize perfluorocarbon (PFC) emissions generated during anode effects in the electrolytic cells at aluminum smelters in China.

Dr. Alton Tabereaux is a technical consultant in resolving issues and improving productivity at aluminum smelters since 2007. He worked for 33 years as a manager of research and process technology for both Reynolds and Alcoa Primary Metals. He was recipient of JOM Best Technical Paper Award in 1994 and 2000, editor of Light Metals in 2004, and received the TMS Light Metals Distinguished Service Award in 2007. He has been a lecturer at the annual International Course on Process Metallurgy of Aluminium held in Trondheim, Norway, and an instructor at the annual TMS Industrial Aluminum Electrolysis Courses. He has published over 65 technical papers and obtained 17 U.S. patents in advances in the aluminium electrolysis process. He participated as a consultant in an EPA sponsored “Asian-Pacific Partnership” program to minimize perfluorocarbon (PFC) emissions generated during anode effects in the electrolytic cells at aluminum smelters in China.

Editor’s Note: This article first appeared in the August 2021 issue of Light Metal Age. To receive the current issue, please subscribe.